I don’t see the prospects for TIPS insurance the same way—I’m more optimistic that TIPS can insure the SPIA for a reasonable cost.McQ said:By referring to TIPs as an "insurance policy" for an SPIA, the idea seems to be that the TIPs will offer some degree of hedging to offset the negative impact of high inflation on a nominal annuty: if the real value of an SPIA contract goes down, the real value of a TIPs ladder goes up remains constant. Of course, the amount of TIPs to buy is a crapshoot because the real value that might be required would depend on the future inflation rate - which is an unknown. And the higher the inflation rate, the less offsetting value provided by the TIPs "policy," which is contrary to the point of having that "insurance" in the first place.2. Owners of SPIAs may wish to protect themselves with a TIPS insurance policy: an abbreviated ladder that commences, say, 10 years after the SPIA was taken out, and continues at least to joint life expectancy. Inflation is the ravager of the SPIA.

I personally intend to annuitize some of my TIAA accumulation in my mid-70s.

And I will certainly lay in a stock of long TIPS as reinsurance on that “insurance” purchase.

...

But, chastened by #Cruncher’s earlier correction, let me lay out my thinking for you to criticize or rebut.

Topic: TIPS bought to insure the real value of SPIA payments.

Simplified assumptions:

1. Couple in their mid-70s have a joint life expectancy of twenty years more or less.*

*rounded value from IRS tables, NOT SSA tables -- “annuitant life expectancy”

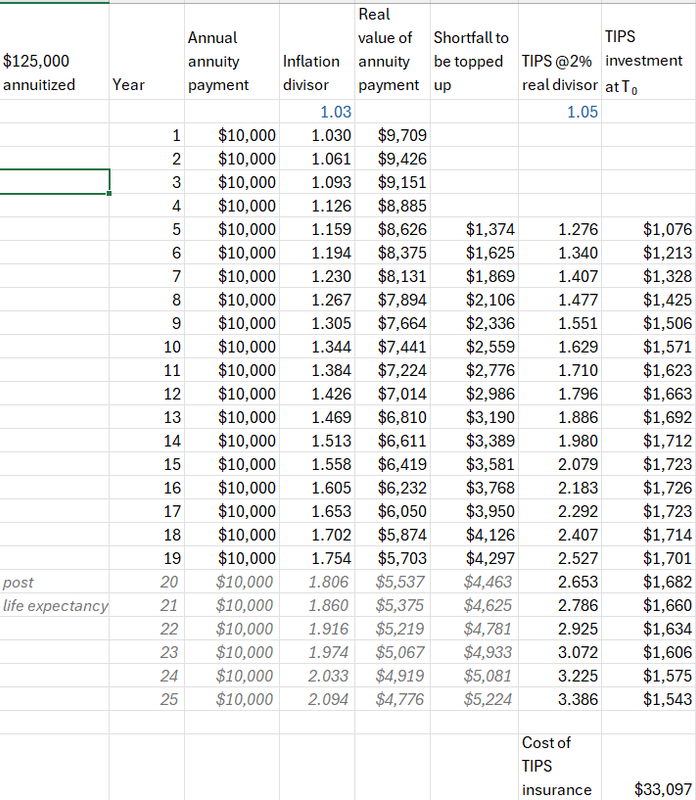

2. If the insurance company is crediting about 5%, annual payments on a premium of $125,000 will be about $10,000.

3. Suppose the inflation expectation is about 3% when the annuity is taken.

4. Long TIPS might then reasonably offer a real yield of 2%.

Next, the annuitants understand that everything is uncertain. They might outlive their life expectancy, say by 5 years. Inflation could be much more than 3%, but probably not much less.

They decide to begin insuring their annuity payments after 5 years, and continue for 5 years after their life expectancy.

Here is how it looks in table form, if inflation conforms to expectation of 3%, more or less, throughout the illustration. (3% = post-1926 US average).

1.After five years of inflation at 3%, the $10,000 payment has lost $1,374 in spending power.

2.A TIPS earning inflation + 2% will have turned $1000 into $1,276 after five years.

3.Therefore, $1,076 of TIPS maturing in five years must be purchased at the outset to cover the anticipated $1,374 shortfall.

4.As inflation continues, more purchasing power is lost, $3,000 after 12 years, $4,000 after 17 years, $5,000 after 23 years.

5.But any TIPS bond purchased at the outset continues to increase in value at inflation + 2%. Therefore, the peak purchase of TIPS occurs for insurance near year 15. After that point, the value of the annuity payments has already been reduced so much that further dollar reductions get smaller and smaller, even as the dollar value of a TIPS adds up faster and faster.

Result: it costs $33,000, somewhat more than one-fourth the amount annuitized, to insure the real value of the SPIA payments for years 5 – 25.

Ah, but we don’t know what future inflation will be!

And the fear, which drives the insurance motive to buy long TIPS, is precisely that inflation will come in high. Frighteningly high.

Let’s play that scenario out next.

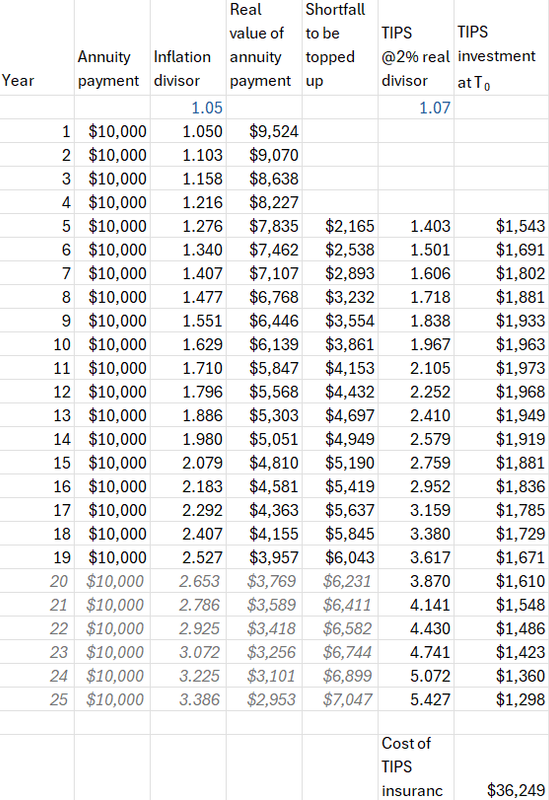

Inflation at 5%

Really? How plausible, here in the great US of A, is 5% inflation sustained for two-and-a-half decades?

Very plausible. EVERY 25-year period beginning from 1956 through 1974, ending 1981 through 1999, saw annualized consumer price inflation above 5%. Some of us are old enough to remember.

Here is the same table, but with TIPS earning 2% more than 5% inflation.

Interesting. The insurance becomes a little more expensive, but the effects of compounding at a higher rate are such that the heavier early year top-offs are partially balanced by the reduced top-offs later on.

The point

TIPS return inflation plus their real yield, regardless of what inflation turns out to be.

I’ve set up the illustration so that whatever happens to the annuity payments, in terms of inflation reductions, also happens to TIPS, in terms of augmented return.

In practice, I’d round up a little and budget one-third the amount annuitized for TIPS insurance.

Caveats

Remember, I gave only a simplified, stylized demonstration, conceptually sound I hope, but do treat as approximations.

If TIPS yield only 1%, the cost of insurance goes up, by 15 – 20% relative to the illustrations, amounting to something like 35% or more of the amount annuitized. More, if you have to use 0% ibonds.

Which is why I am laying in my supply of long TIPS right now!

I suggest you do likewise.

Conclusion

Remember that insurance costs money. In the examples, if you match 30% of the amount annuitized in TIPS, then you only receive 10/13 of the annuity payments you could have received by annuitizing what instead you reserved in TIPS.

That’s the price of being made proof against inflation in later years.

Good news: relative to an SPIA with an escalator clause, if you die before life expectancy your heirs will have a pile of unmatured TIPS.

As opposed to nothing.

PS: don’t assume long TIPS yielding 2.0%+ will be around forever. If this strategy appeals, then buy TIPS now, even if you won’t be annuitizing for some years.

That’s what I am doing.

Statistics: Posted by McQ — Thu May 16, 2024 10:26 pm — Replies 266 — Views 21120