Do you have a link for these empirical results? Any idea about the time period where the research was performed? And just to clarify: is this a position where you are selling or buying volatility?Also, how can the empirical positive returns from volatility exposure with vertical credit spread be explained, which are well protected on the downside? A vertical credit spread, delta hedged. For example sell 5000 put, buy 4800 put, and also sell ES futures to delta hedge the exposure. Some recently created ETFs do something similar. You have net negative exposure to volatility, at pretty much no significant other risk. If it has consistently positive returns, it seems like an opportunity to make "free" money with little risk in the long run, which should not exist.

The textbooks always show the volatility smirk, where implied volatility decreases with increasing strike price. Like the cartoon shown in the link below, for example:

https://www.investopedia.com/terms/v/vo ... y-skew.asp

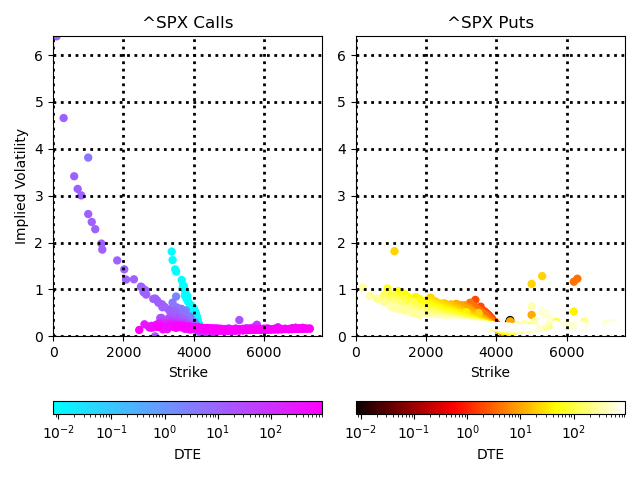

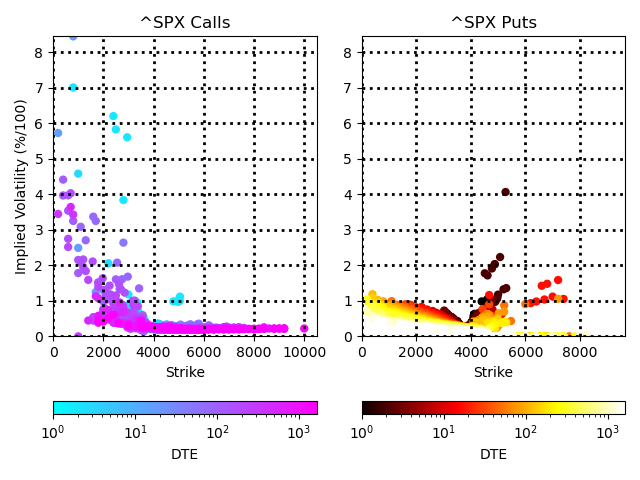

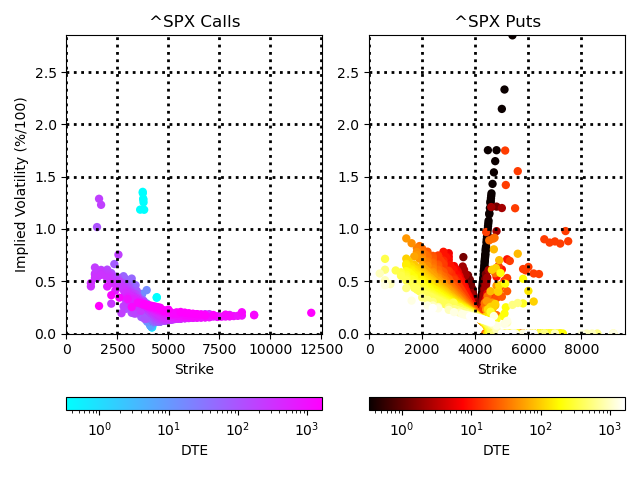

However, this has not quite been what I have observed in SPX options in recent years. Some examples:

SPX-at-time-2021-Jun-07-15-48

SPX-at-time-2022-Jun-28-16-02

SPX-at-time-2023-May-31-07-58:

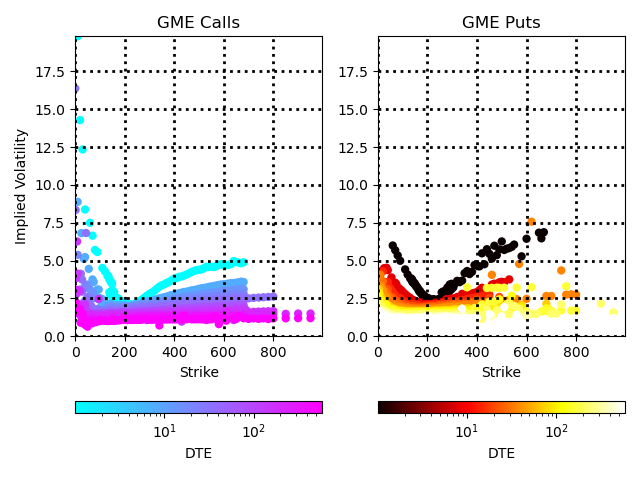

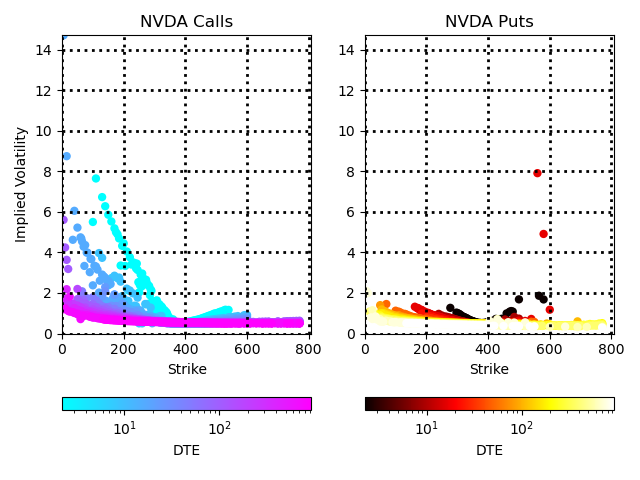

Some single stock examples, where this... non-smirk behavior is more apparent:

GME-at-time-2021-Jun-10-15-52

NVDA-at-time-2023-May-31-10-36

If the "textbook" picture of an implied volatility smirk were true, it would seem that with vertical credit spreads using puts, you would be buying volatility. Because you sell the option at a higher strike and lower IV, and buy the one with a lower strike and higher IV. But, if implied volatility is more "smile-shaped" as in my examples, then you would be selling volatility, because you sell the option at the higher strike having higher IV and buy the one at the lower strike having lower IV.

Edit: I realize now that I was only thinking about the vertical credit spread for strikes above the forward price. I see from your example of 5000 and 4800 that you are probably only referring to OTM put options, with strikes below the forward price. In both the smirk and non-smirk case for OTM put options, the higher strike put always has a lower IV (for strikes below the forward price).

This suggests to me that the position you described is buying volatility. Is this correct?

Statistics: Posted by unemployed_pysicist — Wed Jun 12, 2024 3:06 am — Replies 76 — Views 6541