Thoughts?

![Image]()

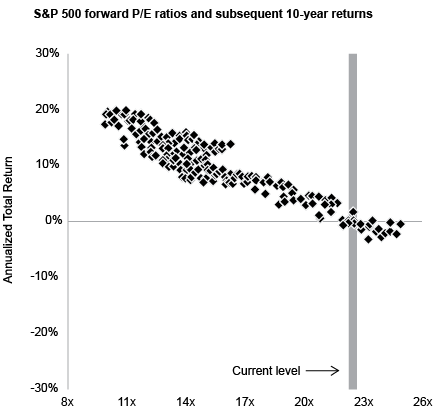

Source:

https://www.oaktreecapital.com/insights ... bble-watch

The graph, from J.P. Morgan Asset Management, has a square for each month from 1988 through late 2014, meaning there are just short of 324 monthly observations (27 years x 12). Each square shows the forward p/e ratio on the S&P 500 at the time and the annualized return over the subsequent ten years. The graph gives rise to some important observations:

There’s a strong relationship between starting valuations and subsequent annualized ten-year returns. Higher starting valuations consistently lead to lower returns, and vice versa. There are minor variations in the observations, but no serious exceptions.

Today’s p/e ratio is clearly well into the top decile of observations.

In that 27-year period, when people bought the S&P at p/e ratios in line with today’s multiple of 22, they always earned ten-year returns between plus 2% and minus 2%.

In November, a couple of leading banks came out with projected ten-year returns for the S&P 500 in the low- to mid-single digits. The above relationship is the reason. It shouldn’t come as a surprise that the return on an investment is significantly a function of the price paid for it. For that reason, investors clearly shouldn’t be indifferent to today’s market valuation.

You might say, “making plus-or-minus-2% wouldn’t be the worst thing in the world,” and that’s certainly true if stocks were to sit still for the next ten years as the companies’ earnings rose, bringing the multiples back to earth. But another possibility is that the multiple correction is compressed into a year or two, implying a big decline in stock prices such as we saw in 1973-74 and 2000-02. The result in that case wouldn’t be benign.

The above are the things to worry about. Here are the counterarguments:

the p/e ratio on the S&P 500 is high but not insane,

the Magnificent Seven are incredible companies, so their high p/e ratios could be warranted,

I don’t hear people saying, “there’s no price too high;” and

the markets, while high-priced and perhaps frothy, don’t seem nutty to me.

* * *

As I said at the start of this memo, I’m not an equity investor, and I’m certainly no expert on technology. Thus, I can’t speak authoritatively about whether we’re in a bubble. I just want to lay out the facts as I see them and suggest how you might think about them . . . just as I did 25 years ago.

I hope you’ll keep reading for the next 25!

January 2, 2025

Source:

https://www.oaktreecapital.com/insights ... bble-watch

The graph, from J.P. Morgan Asset Management, has a square for each month from 1988 through late 2014, meaning there are just short of 324 monthly observations (27 years x 12). Each square shows the forward p/e ratio on the S&P 500 at the time and the annualized return over the subsequent ten years. The graph gives rise to some important observations:

There’s a strong relationship between starting valuations and subsequent annualized ten-year returns. Higher starting valuations consistently lead to lower returns, and vice versa. There are minor variations in the observations, but no serious exceptions.

Today’s p/e ratio is clearly well into the top decile of observations.

In that 27-year period, when people bought the S&P at p/e ratios in line with today’s multiple of 22, they always earned ten-year returns between plus 2% and minus 2%.

In November, a couple of leading banks came out with projected ten-year returns for the S&P 500 in the low- to mid-single digits. The above relationship is the reason. It shouldn’t come as a surprise that the return on an investment is significantly a function of the price paid for it. For that reason, investors clearly shouldn’t be indifferent to today’s market valuation.

You might say, “making plus-or-minus-2% wouldn’t be the worst thing in the world,” and that’s certainly true if stocks were to sit still for the next ten years as the companies’ earnings rose, bringing the multiples back to earth. But another possibility is that the multiple correction is compressed into a year or two, implying a big decline in stock prices such as we saw in 1973-74 and 2000-02. The result in that case wouldn’t be benign.

The above are the things to worry about. Here are the counterarguments:

the p/e ratio on the S&P 500 is high but not insane,

the Magnificent Seven are incredible companies, so their high p/e ratios could be warranted,

I don’t hear people saying, “there’s no price too high;” and

the markets, while high-priced and perhaps frothy, don’t seem nutty to me.

* * *

As I said at the start of this memo, I’m not an equity investor, and I’m certainly no expert on technology. Thus, I can’t speak authoritatively about whether we’re in a bubble. I just want to lay out the facts as I see them and suggest how you might think about them . . . just as I did 25 years ago.

I hope you’ll keep reading for the next 25!

January 2, 2025

Statistics: Posted by babystep — Fri Jan 10, 2025 5:19 pm — Replies 0 — Views 29