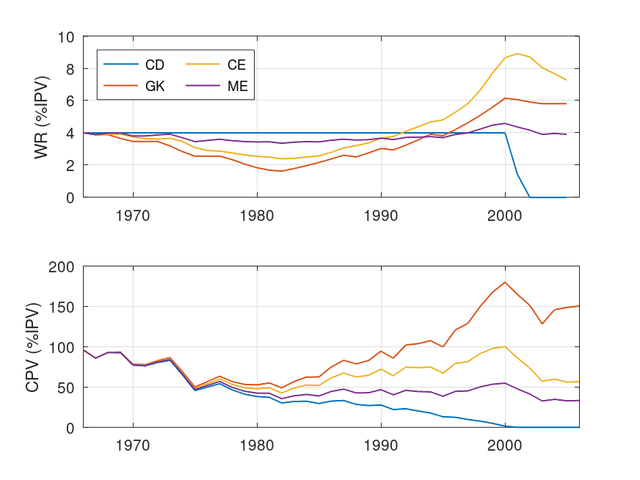

I agree that GK does recognise when portfolio performance deviates from expectations and then adjusts the withdrawals to match. I note that, using the parameters as described in the two papers, GK has a greater flexibility than the F=0.3 I’ve used here. For example, the following graph shows (upper panel) the real withdrawal expressed as a percentage of the original portfolio value and (lower panel) the real portfolio value as a function of time after retirement for a US retirement starting in 1966 (60/40 TSM/TBM portfolio, returns from Simba Rev23b). Four strategies are plotted, CD=constant dollar, GK=Guyton Klinger, CE=Carlson’s endowment, ME=modified endowment (i.e., the version I’ve used in this thread with no feedback). In the latter two cases, the percentage of portfolio used was pmt(3.559%,40,-100,50,1) with percentages capped at 10%, i.e. 4.00%, 4.03%, 4.06%, … 10%, 10%.Flexibility will be critical for many/most retirees if the reductions called out by the Social Security Trustees actually come to pass. I see way too many example of people counting on that fix, and very few alternatives (the most common being ignoring SS entirely).I'd agree - even a small amount of flexibility is useful in terms of portfolio survivability. While I have only covered scenarios where the flexibility factor is fixed, it can also change with circumstances. For example, a very early retiree might adopt a small amount of flexibility before social security kicks in and a greater flexibility afterwards.

Most of the 'hybrid' methods (i.e. those that lie somewhere between SWR and fully percentage of portfolio) are more difficult to implement, but often not excessively so. For example, in the example I've used here you need to calculate both SWR and percentage of portfolio (the same is also true for Carlson's endowment formula and Vanguard's Dynamic Spending Strategy), while with portfolio smoothing you need to calculate the average portfolio size over the last (say) 3 years before then applying a percentage of portfolio. However, IMV, Guyton-Klinger is overly complicated (and the discontinuities in it offend my mathematical sensibilities), but it appears to have a certain level of popularity. I'd agree TPAW has had undergone a lot of thought and effort and is a really practical approach (and the fact that Ben is continually expanding the functionality is great too).

cheers

StillGoing

The biggest benefit I see to GK is that it does attempt to recognize performance deviation from expectations and then manage that deviation.

One of the big concerns I have with SWR methods is that they generally don't match well with what retirees actually need. For example, many need a minimum amount of income, with a hoped-for ability to exceed that. With SWR, that becomes hoped-for portfolio survivability. VPW goes to the opposite extreme, while TPAW is a bit too much leveled-income for me.

I think people should first identify what all they want the retirement portfolio to do, then choose the appropriate way to meet those needs. That almost certainly does not mean to treat it as one big pool. My set of needs are:Those requirements have different time horizons, and different functional requirements which drive specific allocations in the portfolio. The variable income portion is most-closely related to your discussion. I manage that as a perpetuity with a specific targeted growth rate (not exactly typical here).

- Financial Reserves

- Estate Settlement

- Longevity Insurance

- Liability Matching

- Variable Income

- Daily Expenses

- Bequest -- non-specific leftovers in my case

In this example, while constant dollar exhausts the portfolio after nearly 35 years, for each of the flexible strategies, there is money left in the portfolio after 40 years (with GK having the most and ME the least). ME provided an income close to 4% throughout the 40 years (with a mean of 3.8% and a minimum of 3.4%), while both CE (mean=4.4%, min=2.4%) and GK (mean=3.5%, min=1.6%) were more variable (note for CD, the mean=3.5% and min=0%). However, this flexibility means that both CE and GK were more robust to potentially harsher conditions than ME or unexpected longevity.

In my view, your suggestion that “people should first identify what all they want the retirement portfolio to do” is a good one (provided ‘portfolio’ here encompasses ‘all assets’) rather than getting fixated on particular tools (e.g. withdrawal strategies!) since these are a means to an end not an end in themselves. I’d agree, that in your list, ‘Variable income’ is addressed here and that is an important question since the answer should consider both year-to-year flexibility and robustness (since the portfolio going to zero is the ultimate in variable income). For a stock/bond portfolio, the income stream can, on a graded scale, be flexible/robust or fixed/not robust but cannot be ‘fixed and robust').

Out of interest, can you explain “I manage that as a perpetuity with a specific targeted growth rate” in a bit more detail?

cheers

StillGoing

Statistics: Posted by StillGoing — Wed Apr 24, 2024 3:44 am — Replies 17 — Views 2606