Your stock/bond allocation of 100/0 seems fine for a 19-year old, but how would you feel if your IRA value dropped to $3.1K over a few weeks/months, or even overnight (since a -50% stock crash is pretty unlikely, but still feasible)? If you've never taken the time to determine your desired asset allocation (AA), then one or both of the exercises below on "control your risk" level, might be worth pursuing to verify your desired AA (which is the blueprint for managing your long-term & short/mid-term portfolios). There's also a section on int'l diversity suggesting at least 20% of stocks in int'l (e.g., FZILX) or nothing at all since <20% isn't enough for meaningful diversification from a US-only position, which mostly lines up with what @FIRWYW said.I was wondering what I should try to do next; if I should continue contributing to my Roth IRA with the same allocation or if there's other types of investments/accounts I should look into. I'm just looking for any advice or pointers.

Age: 19

Roth IRA: ~$6.2k (90% FZROX, 10% FZILX)

Brokerage: ~$3k (SPAXX) <- I am saving this here for college

On the topic of college savings, I agree with @FIRWYW that borrowing to invest in your future earned income capability is not all-bad, if you pursue a career field that earns well (like significantly higher to you than the median wage of $80.6K from Census 2023) and that you enjoy. I would not suggest anyone pick a major/career just for the potential high salary; I had an older colleague at work that chose engineering and he while he was certainly competent at it, he did seem to actually hate his line of work. I would also not suggest borrowing if you're not going to have a high earnings potential to pay off student loan debt, or you have such an aversion to a large debt balance that you will be miserable & losing sleep every night until it's paid off. There's no one right answer, so you have to decide on investing in your career now (debt) or later (saving up to pay for college partially or fully).

Control Your Risk

1) Read the Wiki article for Assessing Risk Tolerance, take the Vanguard Investor Questionnaire, then tailor the asset allocation (AA) that was recommended by the quiz based on your knowledge of your personal risk tolerance having read the Wiki article.

2) Alternatively (or in addition to), ask "How much of a drop in portfolio value as a % of total value can I handle?" cut that % in half to get standard deviation, then lookup that std. dev. on the X-Axis of the chart below, and finally scan up to see what AA that corresponds to. As an example, if you can only stomach a -24% drop in portfolio value, that's a ±12% std. dev, which corresponds to an AA of 60/40. The return you get is an average and you'll get what you get with your unique sequence of returns (there's a lot of variance in outcomes due to the associated volatility of stocks so it probably will NOT be the average, but something more or less).

a. For a long time-frame (>10 years) AAs below 20% stock are dominated (red dots) by another AA with similar risk but higher reward (blue dots).

b. The dotted line represents a hypothetical linear risk-reward from 100% stocks down to 100% bonds; the historical risk-reward curve has an improvement for risk-adjusted return due to the lack of correlation between stocks & bonds.

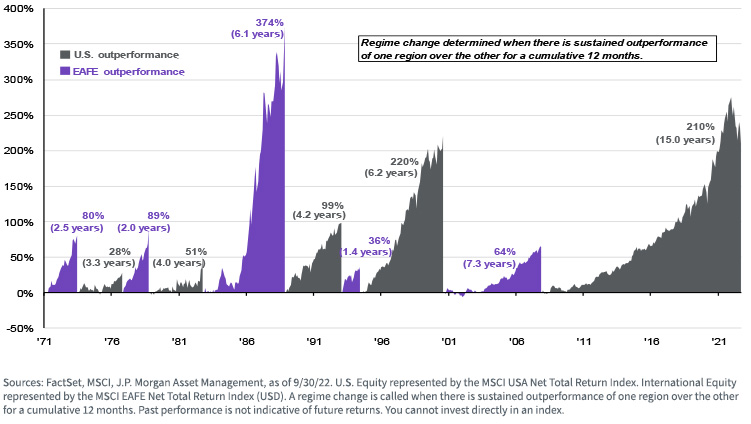

Value of Int'l Diversity from US

There's essentially two camps among Bogleheads: a) Those that are on board with the global market cap weighting, which is about 60% US stock and 40% ex-US stock; and b) those that have a home bias (US will usually outperform), which is about 80% US stock and 20% ex-US stock (some even omit Int'l altogether). I'm in camp a) based on the chart below from WisdomTree, the white paper from Vanguard, and the more recent article from Vanguard.

Vanguard White Paper: International Equity - Considerations and Recommendations

Vanguard Web Article: Making the case for international equity allocations

Applies to bonds too... (when you eventually add those to your desired AA)

Vanguard White Paper on International Bonds

I asked Taylor, author of the 3-Fund Portfolio, about why int'l bonds were omitted and while I expected something about currency risk or higher default risk, relative to the expected reward, instead the response in a private message on 31-Jan-2025 was "I feel simplicity is more important than more diversification."

One could have it all with VT (Van World Stock) and BNDW (Van World Bond), so just two funds, but those are best used in Trad or Roth accounts, not in a Taxable account (and bonds in a Roth is sub-optimal so VT in Trad & Roth, but BNDW only in Trad).

Statistics: Posted by bonesly — Mon Sep 08, 2025 11:12 am — Replies 4 — Views 591